Key Takeaways

- Verification is Mandatory: Kalshi is a CFTC-regulated exchange, meaning withdrawals require strict identity and bank verification that can delay access to funds.

- Settlement vs. Balance: Funds are only withdrawable after a market officially settles; active positions are locked capital until the event resolution.

- Systemic Friction: Fees (like the 2% debit charge) and "recurring" labels on deposits often trigger bank-side blocks or internal platform delays.

- Sovereignty as a Solution: The frustration of "stuck funds" highlights the risks of centralized custody, driving many toward non-custodial financial alternatives.

The Kalshi Withdrawal Reality: Why Your Money Feels Stuck

For many retail traders in the United States, the initial excitement of predicting event outcomes—ranging from Federal Reserve rate hikes to cinematic awards—often hits a brick wall at the exit ramp. You’ve made your trades, the market has closed, and the "Profit" column looks promising. Yet, when you attempt to move that digital balance back into your real-world bank account, the experience can shift from a seamless financial exercise into a bureaucratic nightmare.

User reviews frequently highlight a jarring disconnect: deposits are near-instant, but withdrawals are often mired in a "3-day verification" loop or, in worse cases, seem to disappear into a black hole of "pending" statuses. This friction is rarely an accident. As a regulated entity, Kalshi must navigate the complex web of CFTC regulation, which imposes rigorous anti-money laundering (AML) and Know Your Customer (KYC) standards. While these rules are designed to prevent fraud, they often manifest as "verification traps" that leave users feeling like their capital is being held hostage by a centralized gatekeeper.

The frustration is palpable on platforms like Trustpilot, where traders describe a "nightmare" of unresponsive support and funds that remain "unsettled" long after an event has concluded. To navigate this, one must understand that Kalshi is not a wallet; it is a regulated clearinghouse where every dollar is tracked, verified, and—unfortunately for the impatient—frequently scrutinized before release.

💡 Trader's Reality: "Pending Review" is code for "You don't own your money." In decentralized finance, no one can review your withdrawal because no one holds your funds but you. Learn why custody matters in DEX vs. CEX: Finding the Ultimate Battleground for Solana Scalpers.

Step-by-Step Guide: How to Withdraw from Kalshi Correctly

Navigating the withdrawal process on a regulated exchange requires more than just clicking a button. To ensure your funds aren't caught in digital limbo, you must follow the technical steps precisely while anticipating potential settlement hurdles.

The Technical Withdrawal Process

Before you can initiate a transfer, you must ensure your funds are "settled." Users should always check the "Timeline and Payout" section on the specific market page to confirm the resolution date. Your balance will only reflect withdrawable funds once the market has officially closed and the settlement period has concluded.

Once your funds are available, follow these steps:

- Navigate to the Transfer Section: Log into your account and locate the "Transfer Funds" or "Withdraw" option within your account dashboard.

- Select Your Withdrawal Method: Kalshi typically offers three primary avenues:

- ACH Transfer: The most common method. While ACH deposits are free, withdrawals incur a flat $2 fee.

- Wire Transfer: Recommended for larger sums, though your receiving bank may charge additional incoming fees.

- Crypto (USDC): Kalshi allows for USDC withdrawals via connected wallets, catering to those seeking faster digital settlement.

- Enter Amount and Confirm: Input the amount you wish to withdraw. Ensure you have accounted for the $2 transaction fee to avoid balance errors.

- Verification Check: You may be prompted to re-verify your identity or link your bank account via Plaid if the connection has timed out.

⏳ The "Settlement" Timeline

| Stage | What Happens | Typical Wait Time |

|---|---|---|

| Market Resolution | Event ends, outcome verified | 1 - 24 Hours |

| Funds Settled | Money moves from contract to balance | 1 Business Day |

| Withdrawal Review | Kalshi approves the transfer | 1 - 3 Days |

| Bank Processing | ACH transfer clears | 3 - 5 Days |

| Total Time | From Win to Wallet | 5 - 9 Days |

Why Withdrawals Fail: Fees, Glitches, and 'The House' Advantage

Navigating the withdrawal verification process often feels like a gauntlet designed to keep capital within the platform's ecosystem. While Kalshi markets itself as a regulated alternative to offshore exchanges, users frequently encounter systemic friction when attempting to exit positions.

The Hidden Friction: Fees and Labeling

One of the most significant hurdles is the aggressive fee structure. Many users report a 2% debit fee on transactions, a cost that eats directly into trading margins. More concerning is the trend of "recurring" charge labeling. When a platform utilizes sophisticated payment orchestration, the goal is often to maximize "approval rates" for deposits while introducing "optimal risk management" (friction) for withdrawals.

For the retail trader, this means your withdrawal might be flagged not because of a lack of funds, but because the platform's proprietary engine identifies the transaction as a high-risk event to protect its own balance sheet.

Common Technical and Systemic Failure Points

Withdrawals rarely fail due to a single "glitch." Instead, it is usually a combination of regulatory compliance and deliberate platform limitations:

- Payment Method Mismatches: If you used Apple Pay for a deposit, you may find this method blocked for withdrawals, forcing you into a secondary verification process for a new bank account.

- Settlement Times and Velocity Limits: Centralized platforms often enforce a "one successful withdrawal per 24-hour window" rule.

- The "Recurring Charge" Trap: Some processors label funding transactions in a way that triggers bank-side blocks. If your bank perceives the platform as a subscription service, they may freeze outgoing transfers.

Kalshi vs. Gambling Laws: The Legal Battle Over Your Trades

The safety of your funds is inextricably linked to Kalshi’s legal standing. Unlike traditional stock brokerages, prediction markets sit in a regulatory gray area between financial derivatives and "gaming." This instability directly impacts how and when you can access your money.

Currently, Kalshi is embroiled in high-stakes legal battles that threaten its operational continuity in certain jurisdictions. For example, Connecticut tribes have raised concerns regarding alleged gaming law violations, arguing that these markets infringe upon tribal gaming exclusivity. When a state regulator issues a cease-and-desist, the first thing to be impacted is the withdrawal pipeline.

Furthermore, the CFTC’s ongoing scrutiny of "event contracts"—particularly those involving political elections—means that the rules can change overnight. If a court suddenly rules that a specific market is illegal, your funds could be frozen during the ensuing legal "unwinding" process.

The Case for Sovereignty: Moving Beyond Centralized Gatekeepers

The frustration of learning how to withdraw from Kalshi often stems from a fundamental realization: when your capital is held by a centralized entity, you are not the owner; you are a petitioner. While platforms like Kalshi operate within the bounds of CFTC regulation, that very framework often necessitates the friction—the extended settlement times—that leaves retail traders feeling sidelined.

Embracing the Non-Custodial Future

The evolution of decentralized finance (DeFi) has proven that we no longer need to sacrifice utility for autonomy. We are entering an era where self-custody and regulated infrastructure coexist, allowing for a seamless transition from prediction markets to real-world spending without the "nightmare" of stuck funds.

Key advantages of moving toward a sovereign, non-custodial model include:

- Permissionless Access: You do not need to wait for a manual review from a support desk to move your assets.

- Algorithmic Transparency: Decentralized alternatives operate on publicly verifiable code rather than the "obscurity" of traditional banking ledgers.

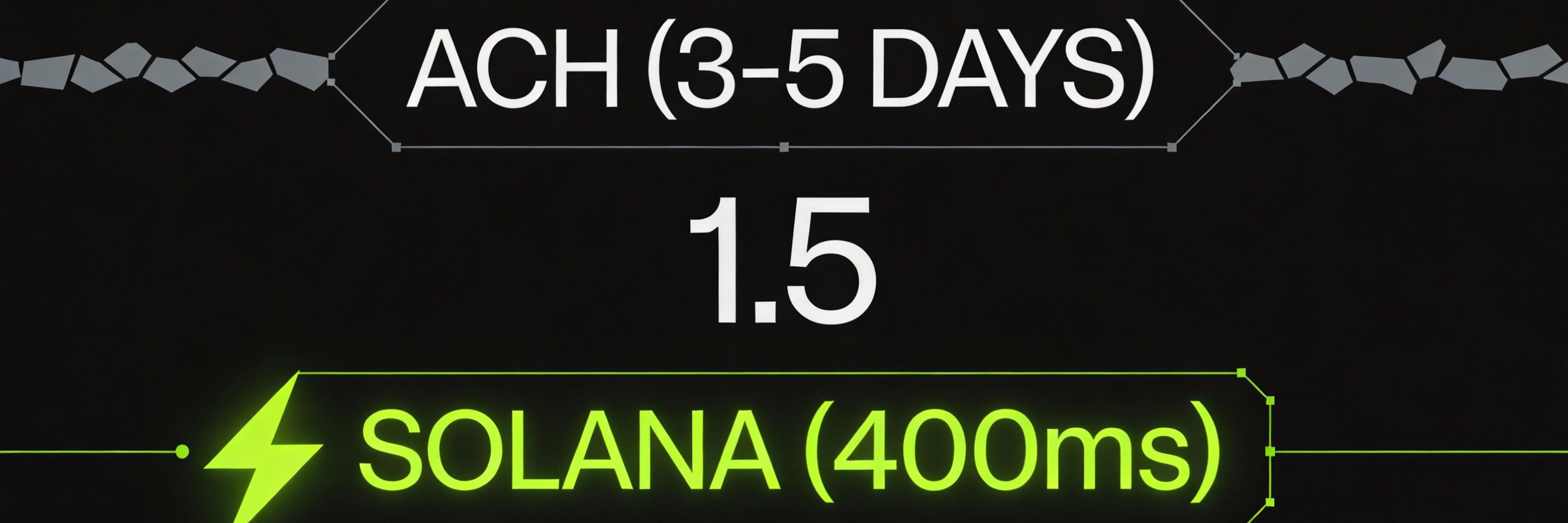

- Direct Settlement: Eliminating the middleman means settlement happens at the speed of the network.

🚀 Update: Prediction Markets Without the Wait

Tired of waiting 5 days for your own money? Manic.Trade offers High-Frequency Prediction Markets on Solana.

- No ACH Delays.

- No "Pending Review" status.

- Instant Wallet Settlement.

Whether you are trading Election odds, Sports, or Gold & Silver prices, your winnings hit your wallet the second the market resolves.

👉 Start Trading Permissionless Prediction Markets on Manic

What to Do If Kalshi Won't Release Your Funds

If you are struggling with how to withdraw from Kalshi or facing unexpected hurdles, you must act decisively. While Kalshi is a regulated exchange, users have frequently reported issues ranging from "glitches" that misplace funds to a verification process that feels like a stalling tactic.

Step 1: Document Everything and Contact Support

Before escalating externally, create a paper trail. According to user reports on Trustpilot, support can be slow, but a documented history is essential for legal escalation.

- Take Screenshots: Capture your account balance and transaction history.

- Email Support Directly: Send a formal request to support@kalshi.com. Include your account ID and the specific withdrawal amount.

- Set a Deadline: State clearly that if the issue is not resolved within 72 hours, you will escalate the matter to regulatory bodies.

Step 2: Seek Financial Sovereignty

The "nightmare" of stuck funds often stems from the centralized nature of these platforms. To avoid the frustration of settlement times that stretch into weeks, many traders are moving toward platforms that prioritize transparency and user-controlled keys.

The bottom line: Do not let your funds sit idle if a platform is ignoring you. Be persistent, document every interaction, and use the regulatory tools at your disposal to ensure your financial sovereignty is respected.

FAQ

1. How long does a Kalshi withdrawal typically take?

Standard ACH withdrawals usually take 3 to 5 business days after the funds have settled. However, if your account triggers a "withdrawal verification process," this can extend to 10 days or more. Wire transfers are faster (1-2 days) but come with higher bank fees.

2. Why is my Kalshi balance showing "unsettled"?

Your balance remains unsettled until the specific event you traded on has reached its official "resolution date" and the clearinghouse has finalized the payouts. This can take anywhere from a few hours to several days after the event ends, depending on the complexity of the market.

3. Does Kalshi charge fees for withdrawing money?

Yes. While ACH deposits are generally free, Kalshi charges a flat $2 fee for ACH withdrawals. Additionally, if you deposited via debit card, you may have already incurred a 2% processing fee that reduces your total withdrawable amount.

4. Can I withdraw my Kalshi funds to a crypto wallet?

Yes, Kalshi supports USDC withdrawals to Ethereum-based wallets. This is often a preferred method for those seeking to avoid the traditional banking system's delays, though you will still need to pass Kalshi's internal verification checks before the crypto transfer is approved.

5. What should I do if my withdrawal has been "pending" for over a week?

First, check your email (including spam) for any KYC or re-verification requests from Kalshi. If there are no requests, send a formal inquiry to their support team with screenshots of the transaction. If you receive no response within 48 hours, consider filing a complaint with the CFPB or the CFTC.

Explore More Trading Resources

Solved your immediate problem? Go deeper:

- Trading Psychology Guide - Why discipline fails and how architecture solves it

- Momentum Trading Guide - Pattern recognition and execution frameworks

- Speed Advantage Guide - Infrastructure that multiplies edge

Browse all resources: Trading Tools & Resources Hub

Ready to trade with zero friction? → Start on Manic.Trade